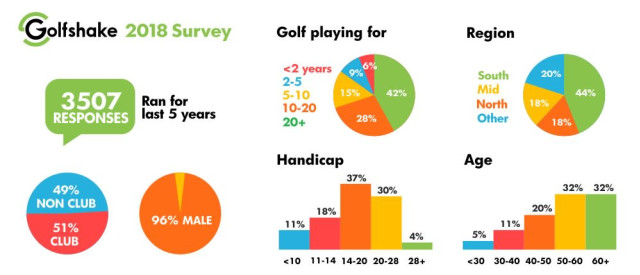

Is the environment more challenging than ever before to successfully run a golf club? When you consider the uncertainty around Brexit and the state of the wider international economy during the past decade, it raises a question further deepened by the changing societial habits and time pressures of modern life, which is packed with distractions in a world that is working and constantly active 24/7. It's a complicated subject that we have explored by analysing data from the recent 2018 Golfshake Survey.

2018 was largely a year to forget in the world of golf. Looking at our golf survey, 18% of respondents stated they had played less golf than in 2017. Work, time and family continue to be the most significant factors when it comes to playing but outside influences also took their toll. 21% of golfers stated injury had stopped them playing more, 19% noted a lack of access to playing partners, 12% said the cost, and the weather accounted for 13% of less rounds due to the cold and 5% due to the hot weather, reflecting the widely contrasting climate that we saw last season in the UK & Ireland.

Visitor green fee revenue

This isn't neccessarily a bad thing with only slightly less golfers overall on the golf course but when analysed further, 21% of non-club members played less, which potentially results in lower green fee revenue for clubs. On a positive note, however, 47% of the non-club golfers are paying on average £20-£30 compared to 44% in 2016/2017, while 8%, compared to 3% previously are now paying £40+ per green fee on average. Furthering this reporting, we asked the golfers surveyed if they were spending more on golf than three years ago - 50% of club members and 63% of non-club golfers stated they were spending more on green fees and 43% and 36% for club and non-club were spending more on food and beverages.

Clubhouse revenue

Access to the clubhouse and ancillary sales highlight a potential further opportunity for golf clubs. The data for the past five years is pretty static with only 37% of non-club golfers visiting the clubhouse after a round, compared with 50% of golf club members. Interestingly, although time is still the largest factor stopping people visiting the clubhouse this is in fact a reversing trend with less stating this reason, and on a positive note for golf in general a factor stopping people four years ago in relation to dress codes is becoming less of an issue with only 6% stating this stopped them compared to 11% in 2014. Not unsprisingly golf club members and golfers over 50 or more likely to visit the clubhouse.

Travelling to play golf

One of the more interesting data sets was around how far golfers are willing to travel for a round of golf. Club members are largely willing to travel further, this may be due to them travelling less in general having a home club, but there was a clear shift in the data from 2016 to 2018. Only 54% of club golfers and 41% of non-club golfers are happy to travel longer than an hour for a round of golf compared to 64% and 53% respectively 2 years ago. Additionally, only 10.8% of club golfers and 6.5% of non-club golfers will travel longer than three hours for a round compared to 15% and 11%. Is this due to the 15-20% cost of travel rises, or further impacts of time on our work, family and social recreational time? Targeting golfers more local can only be a good thing with the opportunity to market return visits and potential membership up sells.

Golf is still great value for money

With all the pressure golf has come under over the last several years, we've seen a drop in some of the green fee prices out there. This has largely been an initiative to encourage visiting golfers, competing with other local courses and as a general marketing tool, but the lowering of prices has been criticised in the past. Ultimately, once you drop the price, can it ever be placed back up? The interesting data coming out of the 2018 survey was the drop in negative responses to the question asked:

"Do you feel the following aspects of the golf industry represents better value for money than it did 3 years ago?"

Prices should rise so it shouldn't always be perceived that things are 'better value for money'. Additionally, the percentage of those stating no potentially highlights that golf is once again heading in the right direction and getting back to where it once was.

Finally, the major positive is that once again 87% would play more golf if they could with golfers under 50 hitting 97%, which probably doesn't come as any surprise when there are key factors preventing that demographic. 78% stated that family/social commitments stopped them playing more and 69% stated time in general. These figures jump right up when analysed 30-50 year old golfers with 98% stating family/social and 81% time in general. So, can more be done to encourage golfers under 50 and families in general to engage with a golf clubs?

That moves us on to the next big question - how do we get more golfers being members of golf clubs? The survey data highllights that potentially 40% of regular avid non club golfers are interested in membership. Read more here.